Accounting is often referred to as the language of business, as it systematically records and communicates financial information. At the heart of this system lies the classification of accounts and the golden rules of accounting, which guide every financial transaction.

Understanding these basic accounting principles helps businesses maintain accurate records, prepare financial statements, and ensure transparency

Meaning of Account

In accounting, an account is a record that summarizes all financial transactions related to a particular item, person, or category. Each account represents either an asset, liability, income, or expense.

For example:

- A Cash Account records all cash transactions.

- A Sales Account records all sales revenue

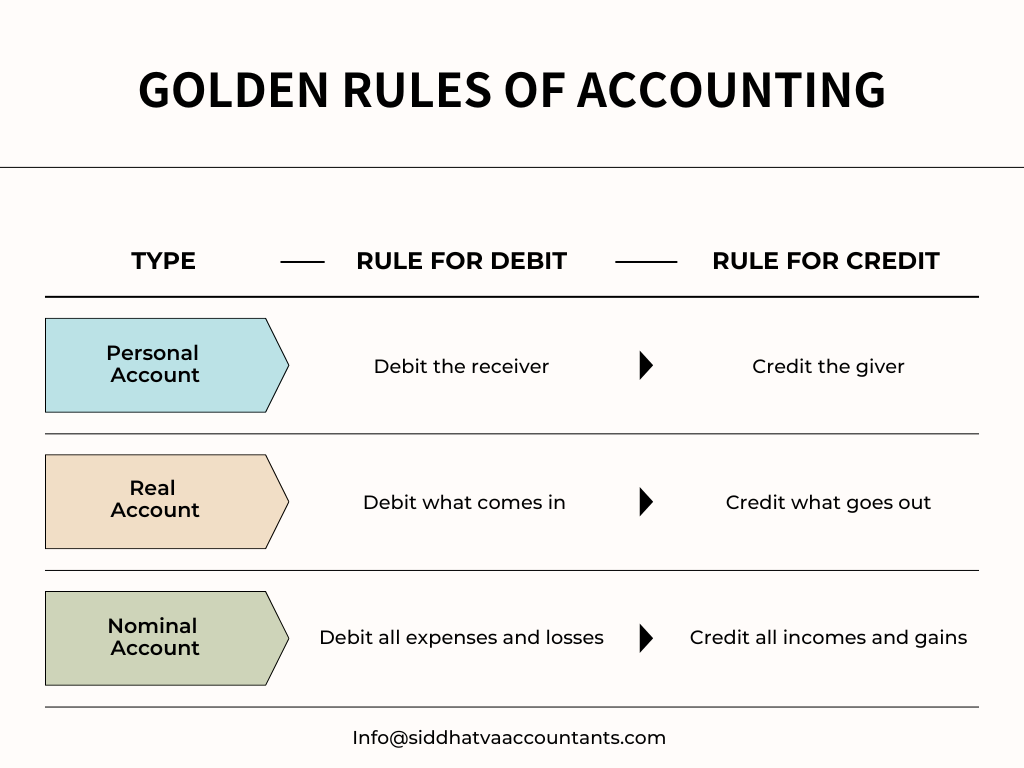

Types of Accounts in Accounting

There are three major types of accounts used in double-entry bookkeeping:

- Personal Account

- Real Account

- Nominal Account

Personal Account

A Personal Account relates to individuals, firms, companies, or any entity with which the business has a financial relationship.

These accounts deal with persons or organizations that owe money to the business or to whom the business owes money.

Types of Personal Accounts

- Natural Persons: Individuals like customers or suppliers (e.g., John’s Account).

- Artificial Persons: Organizations or companies (e.g., XYZ Ltd. Account).

- Representative Persons: Accounts representing a group or category (e.g., Outstanding Salary Account).

Real Account

A Real Account relates to tangible and intangible assets owned by a business. These are permanent accounts that appear on the balance sheet and are carried forward to the next accounting year.

Types of Real Accounts

- Tangible Assets: Physical assets (e.g., Building, Machinery, Furniture).

- Intangible Assets: Non-physical assets (e.g., Goodwill, Patents, Trademarks).

Nominal Account

A Nominal Account relates to expenses, losses, incomes, and gains. These accounts are temporary and closed at the end of each accounting year to determine profit or loss.

Examples of Nominal Accounts

- Expenses: Rent, Salary, Commission

- Incomes: Interest Received, Discount Earned

- Losses: Bad Debts, Depreciation

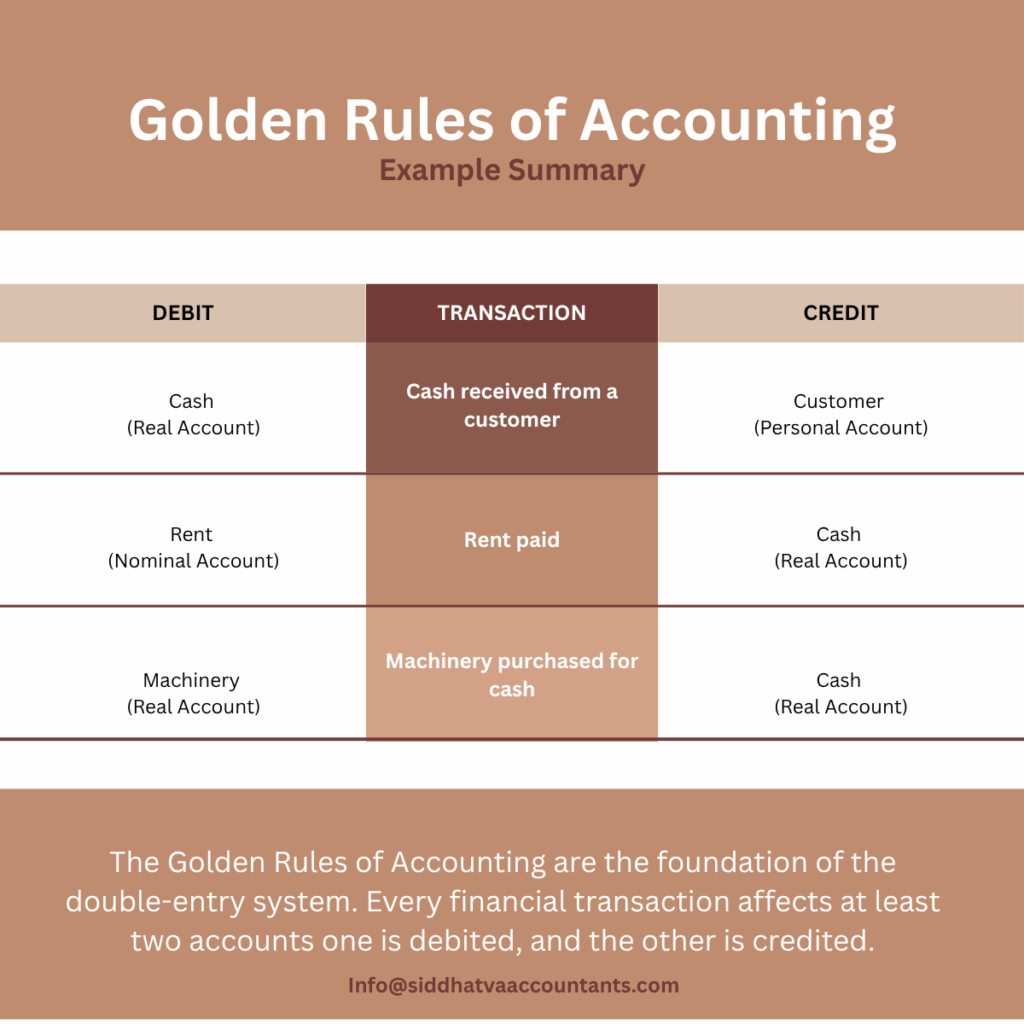

These golden rules ensure that every transaction maintains the accounting equation:

Assets = Liabilities + Equity

Importance of Understanding Types of Accounts

Understanding the types of accounts and their rules is crucial because:

- It ensures accurate recording of transactions.

- It helps maintain the balance in double-entry accounting.

- It supports error-free financial reporting.

- It forms the foundation for advanced accounting concepts.

Conclusion

Accounting may seem complex, but it begins with mastering the three types of accounts: Personal, Real, and Nominal, and applying the Golden Rules of Accounting correctly. These principles form the backbone of every financial transaction, ensuring transparency, accuracy, and consistency in business records.

By following these golden rules, businesses can maintain clear and reliable books of accounts that support better financial decision-making.

Call to Action

Want to build a strong foundation in accounting and maintain accurate financial records?

Connect with us today for expert accounting and bookkeeping services to enhance your business’s financial management.

Balance Sheet Statement

What is a Balance Sheet? A Balance Sheet, also known as a statement of financial position, is a financialreport that…

Profit & Loss (P&L) Statement

A Profit & Loss (P&L) Statement, also known as an income statement, is a financial report that summarizes a company’s revenues,…

Accounting Conventions and Concepts

Introduction A) Accounting Concepts 1. Entity Concept 2. Money Measurement Concept 3. Periodicity Concept 4. Accrual Concept 5. Matching Concept…

Branches of Accounting

Branches of Accounting Introduction Meaning of Accounting Branch Different Branches of Accounting » Financial Accounting » Managerial (Management) Accounting »…

Accrual vs. Cash Basis Accounting

Why Your Business Growth Depends on the Right Choice When it comes to managing business finances, one of the earliest…

Users of Accounting Information

Accounting information is the backbone of every business decision. It provides valuable insights into a company’s financial performance, helping various stakeholders…

Difference between Bookkeeping and Accounting

In the world of finance and business, the terms bookkeeping and accounting are often mentioned together, but they are not the same. Both play…

Types of Accounts and Golden Rules of Accounting

Accounting is often referred to as the language of business, as it systematically records and communicates financial information. At the heart…

Why SMEs Are Turning to Outsourced CFO Services

In today’s fast-paced and unpredictable business environment, small and medium-sized enterprises (SMEs) are under increasing pressure to manage growth, cash…

Why Budgeting Is Essential?

In business, what gets measured gets managed, and budgeting is one of the most powerful tools you have to measure and…

We already have an accountant… why would we outsource?

I hear this from almost every founder we speak with.And it’s a completely valid question. An internal accountant is crucial…

Top 10 Key Advantages of Doing Daily Bookkeeping

In today’s fast-paced business world, financial clarity isn’t optional; it’s essential. Yet, many businesses underestimate the long-term impact of maintaining their books…

Why Outsource Your Accounting & Financial Services?

In today’s fast-paced business environment, companies are constantly seeking ways to increase efficiency, reduce costs, and focus on their core…

The 5 Most Common Financial Mistakes SME Owners Make and How to Avoid Them

Running a small or medium-sized business is no easy task. Between managing operations, serving clients, and leading teams, financial oversight…

How to Manage Accounts Payable Effectively

Accounts Payable (AP) might not grab headlines, but how you manage it can make or break your business cash flow.Poor…

Work Hard? Nah. Work Smart with QuickBooks Online.

Running a small business is no small task. Between managing operations, serving customers, and planning for growth, accounting often gets pushed…

Outsource Your Receivables

Ensure Smooth Payments, Reduce Defaults. Cash flow is the lifeblood of any business, and your receivables process is its heartbeat.…

Master Your Money: Proven Strategies to Control and Manage Business Expenses

Your business isn’t defined by what you earn, but by what you keep.And if you want lasting profitability, there’s one…

What Really Changes When You Outsource Your Accounting

Every business reaches a point where internal accounting processes slow down decision-making, drain valuable resources, and limit strategic focus.And then,…

Why Smart Businesses Outsource Bookkeeping to India?

Breaking Borders, Building Efficiency: Why Smart Businesses Outsource Bookkeeping to India In today’s global economy, success belongs to those who think…

Why Your Business Needs CFO Services Today

In the dynamic world of business, financial expertise can be the difference between success and stagnation. CFO services offer a…

The Power of Effective Accounting for Business Success

In the fast-paced world of business, effective accounting is not just a necessity; it’s a game-changer. Accurate and strategic accounting…

How to Export Lists From QuickBooks Online

In this tutorial, you’ll learn how to export lists from QuickBooks Online. Quick Instructions: Export Customer, Employee & Vendor lists:…

3 Strategies to Boost EBITDA and Drive Value Creation

Private equity (PE) fund sponsors often expect CFOs to play a pivotal role in enhancing EBITDA (earnings before interest, taxes,…

Title: Navigating 2024: A CFO Action Plan for Success

As we step into 2024, CFOs find themselves at the forefront of steering their companies through a landscape marked by…